Unlock Flexible Financing with a Small Business Line of Credit

Flexible Funding Solution: Small Business Line of Credit

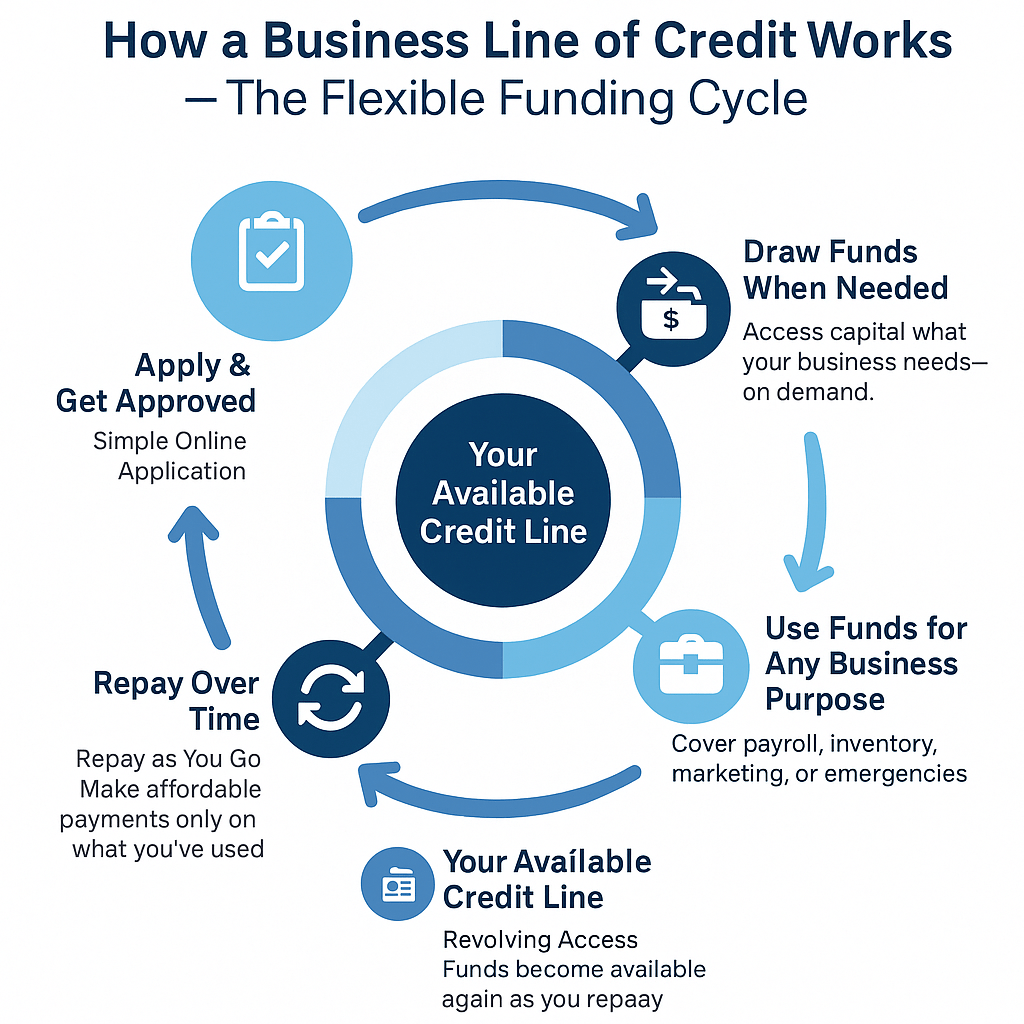

In the dynamic world of small business, cash flow challenges and unexpected opportunities can arise at any moment. A business line of credit offers the financial agility that small businesses need to navigate these situations successfully. Unlike traditional loans that provide lump-sum funding, a line of credit delivers the flexibility to access capital when you need it while paying only for what you use.

Understanding How Business Lines of Credit Work

- Revolving Credit Structure: A business line of credit functions similarly to a credit card but with higher limits and better terms. You're approved for a maximum credit amount—typically ranging from $10,000 to $500,000—but you only draw funds when needed. As you repay borrowed amounts, that credit becomes available again, creating a revolving cycle of accessible funding.

- Interest on Usage Only: The most compelling feature of lines of credit is paying interest only on outstanding balances. If you have access to $100,000 but only use $25,000, you pay interest solely on that amount. When your balance is zero, you incur no interest charges, making it an economical standby financing option.

- Flexible Access Methods: Modern business lines of credit offer various access methods including online transfers, business debit cards, or checks. This convenience means you can access funds immediately when opportunities arise or emergencies occur, without waiting for loan approvals or fund transfers.

Strategic Applications for Small Businesses

- Cash Flow Management: The primary benefit of lines of credit is smoothing cash flow fluctuations. When customers delay invoice payments or seasonal revenue dips create temporary shortfalls, you can draw funds to maintain operations, meet payroll, and pay suppliers without disruption.

- Seasonal Business Support: Seasonal businesses face unique challenges with uneven revenue throughout the year. A line of credit allows retailers to stock holiday inventory in October, landscapers to purchase equipment before spring, or tax preparers to invest in technology before filing season—all while preserving cash flow during slow periods.

- Opportunity Capitalization: When suppliers offer limited-time bulk discounts or competitors liquidate inventory at reduced prices, having immediate access to capital allows you to capitalize on these opportunities. While others wait for loan approvals, you can secure advantageous deals that improve profit margins.

Operational Benefits and Advantages

- Emergency Expense Coverage: Equipment failures, facility repairs, or sudden increases in demand can strain business budgets. A line of credit ensures these unexpected expenses don't derail operations or force you to decline profitable opportunities. This financial safety net provides peace of mind and operational stability.

- Supplier Relationship Enhancement: Consistent, timely payments to suppliers strengthen relationships and often result in better terms, early payment discounts, and priority treatment during supply shortages. A line of credit ensures you never miss these relationship-building opportunities due to temporary cash constraints.

- Professional Image Maintenance: The ability to pay bills promptly and maintain consistent operations projects a professional, financially stable image. This reputation enhances credibility with customers, suppliers, and potential business partners, creating long-term value beyond the immediate financing benefit.

Cost-Effective Financing Structure

- Lower Rates Than Credit Cards: Business lines of credit typically offer interest rates 5-15 percentage points lower than business credit cards. For companies that might otherwise rely on credit cards for working capital, this represents substantial savings over time while providing much higher credit limits.

- Minimal Fees and Charges: Many lines of credit have low or no annual fees, no prepayment penalties, and reasonable draw fees. This cost structure makes them economical for businesses that need standby financing without the expense of maintaining unused traditional loans.

- Scalable Credit Limits: As your business grows and demonstrates responsible credit management, lenders often increase credit limits automatically or upon request. This scalability means your financing capacity grows with your business needs.

Building Business Financial Strength

- Credit Profile Development: Responsible use of a business line of credit helps build your company's credit profile. Regular usage and timely payments demonstrate creditworthiness to future lenders, potentially leading to better terms on additional financing products.

- Financial Discipline Enhancement: Managing a line of credit requires ongoing attention to balances, usage patterns, and repayment schedules. This discipline often improves overall financial management and provides valuable experience in debt management.

- Relationship Building with Lenders: Successfully managing a line of credit establishes positive relationships with financial institutions. These relationships can lead to additional financial products, better terms on future loans, and preferential treatment during economic uncertainties.

Qualification and Application Considerations

- Typical Requirements: Most lenders require at least one year of business operation, minimum monthly revenues of $10,000-$25,000, and reasonable credit scores (typically 650+ personal, 75+ business). These requirements are generally less stringent than term loans, making lines of credit more accessible.

- Documentation Needs: Applications typically require bank statements, financial statements, and basic business documentation. The streamlined documentation process reflects the revolving nature of the credit and reduces approval timelines compared to traditional loans.

Strategic Usage Guidelines

- Use for Short-Term Needs: Lines of credit work best for short-term funding needs rather than long-term investments. Use them for cash flow gaps, inventory purchases, or temporary working capital needs while reserving term loans for major equipment or expansion investments.

- Maintain Conservative Utilization: Keep outstanding balances well below your credit limit—ideally under 30%—to maintain good credit standing and preserve borrowing capacity for genuine emergencies or significant opportunities.

Maximizing Your Line of Credit Value

A business line of credit transforms small businesses from reactive survivors into proactive competitors. The financial flexibility to address cash flow challenges, capitalize on opportunities, and maintain operational excellence provides a significant competitive advantage in today's dynamic marketplace.

By understanding how to use this financing tool strategically and managing it responsibly, small businesses can achieve the financial agility that enables sustainable growth and long-term success.